How Reporting Foreign Inheritance to IRS Functions: Trick Insights and Standards for Tax Reporting

Navigating the intricacies of reporting foreign inheritance to the IRS can be tough. There specify thresholds and forms that individuals need to recognize to ensure compliance. Inheritances going beyond $100,000 from non-resident aliens call for certain focus. Failure to abide by these standards may lead to penalties. Comprehending the subtleties of tax obligation effects and necessary documentation is vital. The adhering to areas will certainly lay out important understandings and standards for efficient tax reporting.

Comprehending Foreign Inheritance and Its Tax Obligation Implications

When individuals obtain an inheritance from abroad, it is essential for them to understand the associated tax obligation ramifications. In the USA, acquired assets are normally not subject to income tax obligation, however the estate from which the inheritance comes might have certain tax commitments. Foreign inheritances can complicate matters, as different nations have differing policies pertaining to inheritance tax. People have to realize that while they might not owe tax obligations on the inheritance itself, they might be in charge of reporting the worth of the foreign possession to the Internal Earnings Solution (INTERNAL REVENUE SERVICE) Furthermore, currency exchange rates and appraisal techniques can influence the reported worth of the inheritance. Comprehending these elements is essential to prevent unforeseen tax responsibilities. Looking for assistance from a tax obligation expert skilled in global inheritance regulations can supply clarity and warranty compliance with both united state and foreign tax obligation needs.

Coverage Demands for Inherited Foreign Possessions

The reporting demands for acquired international possessions involve certain limits and restrictions that taxpayers need to recognize. Conformity with IRS guidelines necessitates the proper tax kinds and understanding of prospective charges for failing to report. Comprehending these elements is essential for individuals receiving international inheritances to stay clear of legal issues.

Reporting Thresholds and Purviews

While going across the complexities of acquired foreign possessions, comprehending the reporting thresholds and limitations established by the IRS is vital for conformity. The IRS requireds that U. reporting foreign inheritance to IRS.S. taxpayers report international inheritances surpassing $100,000 from non-resident aliens or international estates. This limit puts on the overall worth of the inheritance, encompassing all properties obtained, such as cash, realty, and investments. In addition, any type of international monetary accounts amounting to over $10,000 should be reported on the Foreign Checking Account Report (FBAR) Failure to abide by these thresholds can cause substantial charges. It is critical for taxpayers to precisely evaluate the worth of inherited international assets to assure compliant and timely reporting to the IRS

Tax Forms Introduction

Charges for Non-Compliance

Failure to adhere to reporting demands for acquired foreign possessions can result in significant fines for united state taxpayers. The IRS implements rigorous policies pertaining to the disclosure of international inheritances, and failures can result in fines that are often substantial. For circumstances, taxpayers may face a penalty of as much as $10,000 for failing to file Type 3520, which reports foreign presents and inheritances exceeding $100,000. Additionally, proceeded non-compliance can intensify fines, potentially reaching up to 35% of the value of the inherited possession. Additionally, failure to record can also cause much more extreme consequences, consisting of criminal costs for willful forget. Taxpayers have to stay alert to stay clear of these effects by guaranteeing prompt and exact coverage of international inheritances.

Trick Types and Documentation Needed

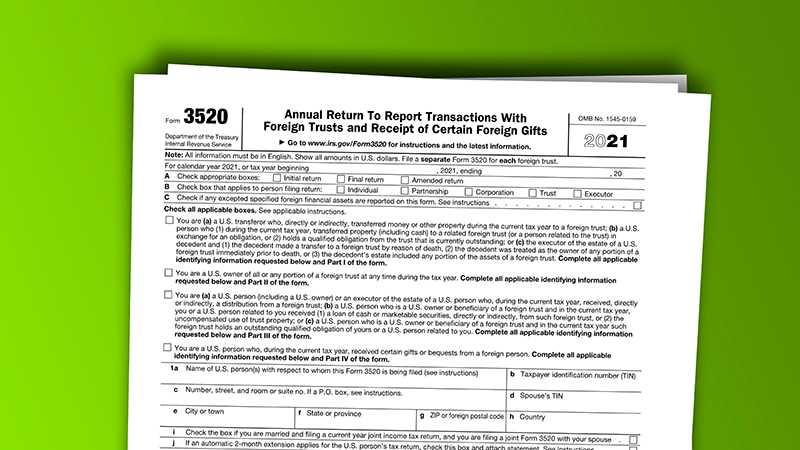

When a private receives an international inheritance, it is vital to understand the crucial forms and paperwork required for compliance with IRS laws. The main kind needed is the IRS Type 3520, which must be filed to report the invoice of the foreign inheritance. This type provides thorough information regarding the inheritance, consisting of the identity of the international decedent and the worth of the inherited properties.

Additionally, if the inherited residential property consists of foreign checking account or various other financial possessions, the person might need to file the Foreign Financial institution Account Record (FBAR), FinCEN Form 114, if the overall worth goes beyond $10,000. Proper paperwork, such as the will or estate papers from the international jurisdiction, should likewise be gathered to confirm the inheritance claim. Keeping complete documents of all communications and deals associated with the inheritance is crucial for exact reporting and compliance with IRS requirements.

Tax Treaties and Their Effect on Estate Tax

Recognizing the effects of tax obligation treaties is vital for individuals receiving foreign inheritances, as these agreements can significantly impact the tax responsibilities related to inherited assets. Form 3520 foreign gift. Tax obligation treaties in between nations commonly give details standards on exactly how inheritances are exhausted, which can result in reduced tax obligation responsibilities or exceptions. As an example, a treaty may stipulate that certain kinds of inheritances are exempt to tax in the recipient's country, or it might permit credit scores versus taxes paid abroad

Individuals need to familiarize themselves with the specific stipulations of appropriate treaties, as they can vary substantially. This understanding aids ensure compliance with tax obligation policies while making the most of possible benefits. In addition, additional resources comprehending how treaties engage with domestic legislations is important to properly report foreign inheritances to the IRS. Subsequently, consulting with a tax obligation professional skilled in international tax regulation may be a good idea to navigate these complicated regulations efficiently.

Common Errors to Prevent When Coverage Inheritance

Although several individuals believe they can conveniently browse the intricacies of reporting foreign inheritances, they typically ignore critical information that can bring about substantial mistakes. One common mistake is failing to report the inheritance in the correct tax year, which can result in penalties. Additionally, some people forget to transform international possessions into U.S. dollars at the appropriate currency exchange rate, ultimately misstating their value. One more frequent oversight entails misunderstanding the reporting limits; people may presume they do not need to report if the inheritance is listed below a certain quantity, which is incorrect. Additionally, misclassifying the type of inheritance-- such as treating a gift as an inheritance-- can make complex reporting commitments. People typically fail to maintain comprehensive documents, which is necessary for confirming cases and preventing audits. Understanding of these mistakes can greatly improve compliance and minimize the risk of monetary effects.

Seeking Specialist Assistance for Complicated Situations

Navigating the details of reporting foreign inheritances can be daunting, especially for those with complicated economic situations. Individuals encountering problems such as multiple foreign possessions, differing tax ramifications across territories, or elaborate household dynamics might gain from professional assistance. Tax professionals focusing on global tax obligation law can supply invaluable understandings into the nuances of IRS regulations, making certain compliance while decreasing possible liabilities.

Engaging a certified public accounting read this post here professional (CPA) or tax obligation attorney with experience in international inheritance can assist clear up reporting needs, identify suitable exceptions, and strategize best tax obligation approaches. They can aid in completing essential types, such as Type 3520, and taking care of any type of extra disclosure demands.

Eventually, seeking expert guidance can alleviate stress and boost understanding, permitting people to concentrate on the emotional aspects of inheritance rather than coming to be bewildered by tax obligation complexities. This proactive approach can bring about extra desirable results in the long run.

Frequently Asked Inquiries

Do I Required to Report Foreign Inheritance if I'm Not a united state Resident?

Non-U.S. people generally do not require to report international inheritances to the IRS unless they have particular connections to united state tax laws. It's advisable to get in touch with a tax professional to make clear individual conditions.

Are There Fines for Stopping Working to Report Foreign Inheritance?

Yes, there are fines for failing to report international inheritance. Individuals might face substantial fines, and the IRS can impose added consequences for non-compliance, possibly impacting future tax obligation filings and monetary standing.

Can I Deduct Expenditures Connected To Taking Care Of Inherited Foreign Assets?

Expenditures related to taking care of inherited foreign properties are typically not insurance deductible for tax functions. People ought to seek advice from a tax obligation professional for assistance tailored to their details circumstances and prospective exemptions that might use.

Just How Does Foreign Currency Affect the Value of My Inheritance Record?

International money variations can significantly affect the reported worth of an inheritance. When transforming to united state dollars, the currency exchange rate at the time of inheritance and reporting identifies the final reported value for tax functions

What Occurs if My International Inheritance Is Kept In a Trust?

If a foreign inheritance is held in a trust, it may make complex coverage needs. The trust fund's framework and tax obligation effects have to be assessed, as recipients can face differing tax obligations based upon territory and trust kind.

The IRS mandates that United state taxpayers report international inheritances surpassing $100,000 from non-resident aliens or international estates. In addition, any foreign monetary accounts amounting to over $10,000 should be reported on the Foreign copyright Report (FBAR) People acquiring foreign assets have to typically report these on blog Type 8938 (Declaration of Specified Foreign Financial Possessions), if the total worth surpasses certain limits. Depending on the nature of the inheritance, various other forms such as Kind 3520 (Yearly Return To Report Purchases With Foreign Trusts and Receipt of Certain International Gifts) might likewise be necessary. In addition, if the inherited building includes international financial institution accounts or other economic assets, the person may require to file the Foreign copyright Record (FBAR), FinCEN Form 114, if the complete value goes beyond $10,000.